Water Matters 2026

Foreword

Our Water Matters tracking survey is now in its fifteenth year, and it continues to give us invaluable insights into household customers’ views and preferences on water companies’ services across England and Wales. This makes it one of the most comprehensive records of customer views and preferences across any utility.

Despite some green shoots of recovery in last year’s Water Matters from the record low results we saw in the 2024 edition, we have seen a renewed decline in customer perceptions across the board, with long-term trends remaining downward. The signs of trust being rebuilt by the majority of companies last year have not been sustained, although some saw steeper declines than others.

Fewer customers said they were satisfied with the value for money of the services they receive and whether water charges are fair. Of particular concern is the significant decline in customers feeling their charges are affordable. Perhaps this is not surprising as fieldwork was carried out after charges increased by a record amount in April 2025, with the average household water and

sewerage bill increasing by 26%.

While it was disappointing to see a drop in how well companies communicate their services, it is encouraging that awareness of affordability support has significantly increased from 49% to 56%. This has exceeded our 2025/26 Forward Work Programme target of 53% awareness by summer 2026. It is vital that companies continue to promote the support on offer.

Against a backdrop of higher charges and affordability concerns, it is more important than ever that customers are aware of the financial assistance companies can offer.

We also saw a further increase in the number of customers contacting their company, exceeding the previous record set in last year’s report. This was paired with a decline in overall satisfaction with contact. At a time when trust and satisfaction with services are declining, companies need to be doing all they can to resolve customer queries, as well as improving their contact handling.

Overall, it is worrying that downward trends are continuing. Changing customer perceptions can take time, but a lot more work is needed by companies to turn things around. It is not acceptable to see a further move in the wrong direction. Companies need to significantly increase their efforts to regain trust and improve both the communication and delivery of services.

This year saw the launch of our Water Voice consumer panels1, which allow customers to hold their water company directly to account. Views and concerns expressed in the accountability sessions held so far correlate with the findings in this report around communication and billing queries. Where we see common themes emerging between our research and the consumer panels, this provides companies with an even greater understanding of what their customers care about and what needs to improve. If customers feel they are being listened to and can rely on their company to be there when they need them, then this will go a long way to restoring trust and satisfaction in a number of key metrics.

1 The consumer panels allow around 50 customers of each water company to take part in regular research to share their views on their company. A smaller number also attend Accountability Sessions where they can directly challenge their company’s senior executives on the issues that matter most to them, such as affordability, environmental performance and customer service.

Key numbers for England and Wales

- 6.07 out of 10 – average water company trust score, down from 6.28 (record low)

- 63% – agree that water and / or sewerage charges are affordable, down 11% (record low)

- 60% – overall satisfaction with sewerage services, down 4% (record low)

- 86% – overall satisfaction with water supply, down 4% (record low)

- 51% – agree that their water company cares about the service it provides, down 2%

- 57% – satisfaction with value for money of water services, down 9% (record low)

- 62% – satisfaction with value for money of sewerage services, down 5% (record low)

- 44% – agree the charges they pay are fair, down 9% (record low)

Key learnings

The improvements we saw last year have not been sustained

While longer-term trends remained negative, in last year’s Water Matters we saw some improvements in key metrics – such as whether customers think their company cares about the service it provides and overall satisfaction with water services – from the record fall we saw in our 2024 report. However, these tentative signs of recovery have not been maintained. Customer perceptions have declined across the board with new record lows now being seen in trust, and satisfaction in both water and sewerage services.

The latest results show that the issue of falling trust and satisfaction has been sustained and can no longer be attributed to a minority of companies performing poorly. Most companies have seen trust and satisfaction reduce, in stark contrast to last year’s report when it was only the steep declines from a minority of companies that brought down the overall score.

Customer contact with water companies has increased again, breaking the previous record set last year

We saw another increase in the number of customers contacting their water company, with the number of contacts about billing enquiries also increasing. Billing remains the main driver for contact to companies, which is also reflected in customer complaints. It is not surprising to see this after households were hit with a record increase in water bills from April 2025. While slightly improved from our previous report, nearly 40% of customers in England and Wales think their financial situation has changed for the worse since last year.

Alongside the increase in those contacting their company, the number who were satisfied with the contact significantly decreased. This is another area where the lowest scores in Water Matters history have been recorded. Companies need to take steps to improve their contact handling, particularly if the level of customer contact continues to rise.

Awareness of support for households, including WaterSure and Priority Services, is now at its highest ever level – as is concern about the affordability of bills

The number of customers that agree their charges are affordable has declined to its lowest ever level (down from 74% to 63%), against the backdrop of the record bill rises we saw in April 2025. Satisfaction with value for money, for both water and sewerage services, also continues to decline. However, awareness of the financial support that companies offer has risen to record levels, from 49% to 56%. It is more important than ever that customers know what help is available and companies continue to actively promote this.

Awareness of Priority Services2 has also increased to a record high – 55% to 59%. Some of the high-profile supply interruptions we saw throughout the past year have highlighted the importance of vulnerable customers having access to the support they are entitled to in an emergency. We know from additional customer research that there is a strong level of satisfaction with Priority Services from those already registered. Companies must keep promoting this service effectively so vulnerable customers have access to the support they need, when they need it most.

2 The Priority Services Register (PSR) is a free support service for customers needing extra help due to age, ill health, disability, mental health issues, or young children. Benefits include advanced notice of supply interruptions, priority support during incidents (e.g. bottled water delivery), and tailored communication

Detailed findings

1. Negative long-term trends continue, with a reversal of the previous small improvements

We continue to see negative ten-year trends across a range of areas – such as care, trust, and overall satisfaction with water and sewerage services – that had been stable prior to 2024.

Our previous report showed the ten-year trends turning negative for the first time in traditionally higher-performing Wales. With the exception of customer satisfaction with value for money of water and sewerage services, these downward trends have continued in key areas such as care (see below), and trust.

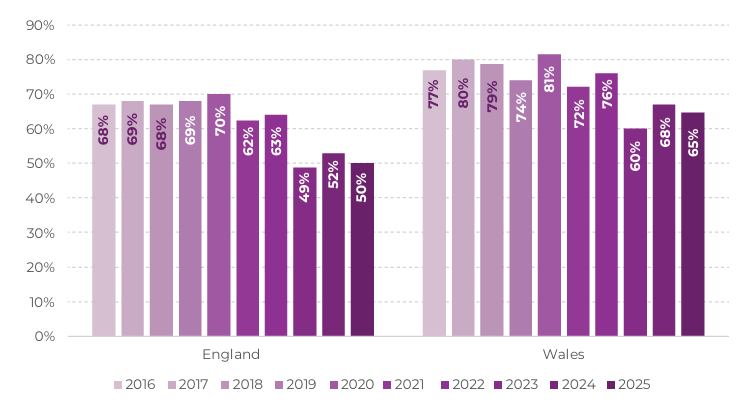

Despite the number still being well below those prior to 2024, the small improvement we saw in last year’s report in the number who agree their company cares about the service it provides was welcome. However, as the below chart shows, a sustained recovery has not materialised.

Last year, we saw a degree of regional variation in customer views, with a minority of companies seeing steep declines. This resulted in the overall score going down, despite improvements by a significant number of other companies. We have seen something similar this year in care and satisfaction with sewerage services, where a handful of poor performers have driven the overall decline in average scores.

Most companies have failed to build on last year’s improved trust scores. In fact, 13 saw a reduction, with Southern Water and Yorkshire Water seeing the biggest declines, resulting in the overall score across England & Wales falling from 6.28 to 6.07 – another record low.

Table 1 shows each company’s performance in relation to trust compared to the previous year: companies in green improved their trust score, while companies in red saw a further fall. Customers’ overall satisfaction with sewerage services has sunk to its lowest ever level. Their biggest concerns in this area continue to be companies’ failure to minimise sewer flooding and not cleaning wastewater properly before releasing it back into the environment. However, there was regional variation with almost half of companies improving their overall satisfaction with sewerage services from the previous year. The average fell due to the significant decline in scores of a small number of companies – in particular, Thames Water (down 14%, to 44% of customers satisfied) and Yorkshire Water (down 8%, to 57%).

Customer satisfaction with the value for money water companies provide is now at a record low – standing at 57% for water and 62% for sewerage. Customer satisfaction with their water and sewerage services continues to decline, so this finding is not surprising. Concerns around value for money have also been expressed during our consumer panel sessions, with customers wanting more information on how their money is being spent. Companies need to do more to explain to customers why charges have increased and what this is delivering in return. We have explored this in further detail in our recent research: The Bottom Line: Helping customers understand water company finances.

Figure 1: Agreement that your water / water and sewerage company cares about the service it provides to customers, England vs Wales, 2016-2025

Table 1: Changes in trust by company

| Company | 2024 | 2025 | Change from last year |

|---|---|---|---|

| Southern Water | 5.74 | 5.08 | -0.66 |

| Yorkshire Water | 6.50 | 5.96 | -0.54 |

| Thames Water | 5.12 | 4.74 | -0.38 |

| United Utilities | 6.57 | 6.23 | -0.34 |

| South West Water | 5.42 | 5.13 | -0.29 |

| Cambridge Water | 6.77 | 6.50 | -0.27 |

| Dwr Cymru Welsh Water | 6.86 | 6.66 | -0.2 |

| South East Water | 5.81 | 5.64 | -0.17 |

| Severn Trent Water | 6.61 | 6.45 | -0.16 |

| Wessex Water | 7.02 | 6.87 | -0.15 |

| Portsmouth Water | 6.83 | 6.68 | -0.15 |

| Affinity Water | 6.46 | 6.41 | -0.05 |

| Anglian Water | 6.46 | 6.45 | -0.01 |

| Essex & Suffolk Water | 6.81 | 6.89 | 0.08 |

| Northumbrian Water | 6.91 | 7.02 | 0.11 |

| SES Water | 6.63 | 6.76 | 0.13 |

| Hafren Dyfrawy | 6.80 | 6.98 | 0.18 |

| Bristol Water | 6.70 | 6.90 | 0.2 |

| South Staffs Water | 6.70 | 6.95 | 0.25 |

2. Company contact and Communication

The number of people who have contacted their company over the last 12 months has increased again – up to 28%, breaking the previous year’s record. Wales saw a particularly Cymru Welsh Water and Hafren Dyfrdwy saw some of the biggest declines in the number of customers who believe their charges are either fair or affordable, which could account for the overall increase in customer contact in Wales.

While customer contact to water companies reached a record high, satisfaction with this contact reached a new low. This continued the downward trend in satisfaction seen over the last ten years. As was the case in most previous years, satisfaction with ‘the way you were kept informed of progress’ is the lowest of the different elements of contact. However, the biggest decrease was those who felt their ‘contact had been/would be resolved’ – falling from 75% to 68%. Companies should prioritise improving the quality of outcomes and the way they communicate with customers to try and improve their overall satisfaction scores.

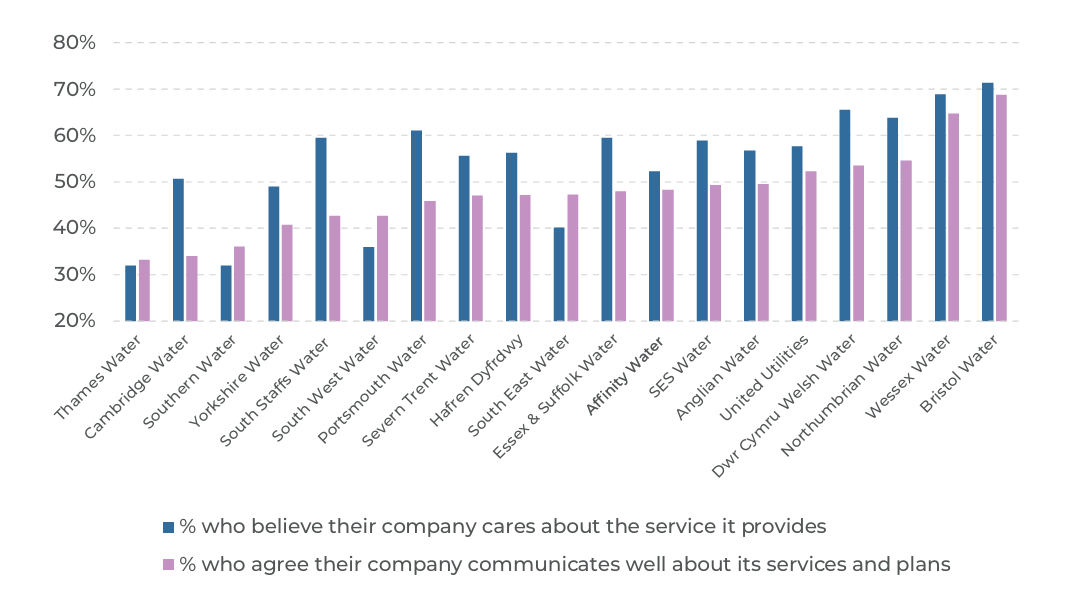

Last year’s report showed an uptick in how well customers felt their company communicated plans and services, so it is disappointing to see this fall back to the low we saw in 2024. The vast majority (70%) of those who were dissatisfied with communication said they either don’t receive regular correspondence from their company, or don’t recall seeing anything apart from their bill. This is also a theme from the consumer panel sessions where customers say a lack of clear and proactive communication is hindering their understanding of bills and the support on offer. This should provide extra motivation to companies to improve their overall communication, particularly as there is also a correlation between how well customers feel their company communicates and whether they think the company cares about the service it provides.

Billing queries continued to account for the majority of customer contacts to their company, and there was no change in the percentage who got in touch due to being worried about their bill. Regional variability has also reduced since last year with most companies seeing an increase in these areas. With more customers than ever contacting their company, a concerted effort is needed to make sure all queries are dealt with effectively. After the record bill rises in April 2025, customers will be paying more attention to their charges, and many will want to know what payment support is on offer. Companies providing customers with all the information they need in a timely manner will go a long way to restoring lost satisfaction and trust.

Figure 2: Proportion of customers who believe their company cares about the service it provides, against satisfaction with communications

3. Concerns with bills and support measures

Customer perceptions of value for money for water and sewerage services, fairness of charges, and affordability of charges have all significantly decreased. It is important to note that fieldwork took place after the record bill rises in April 2025, so the findings are likely a reflection of this. This is further supported by billing enquiries accounting for an even larger proportion of customer contacts to companies – up from 33% to 37%.

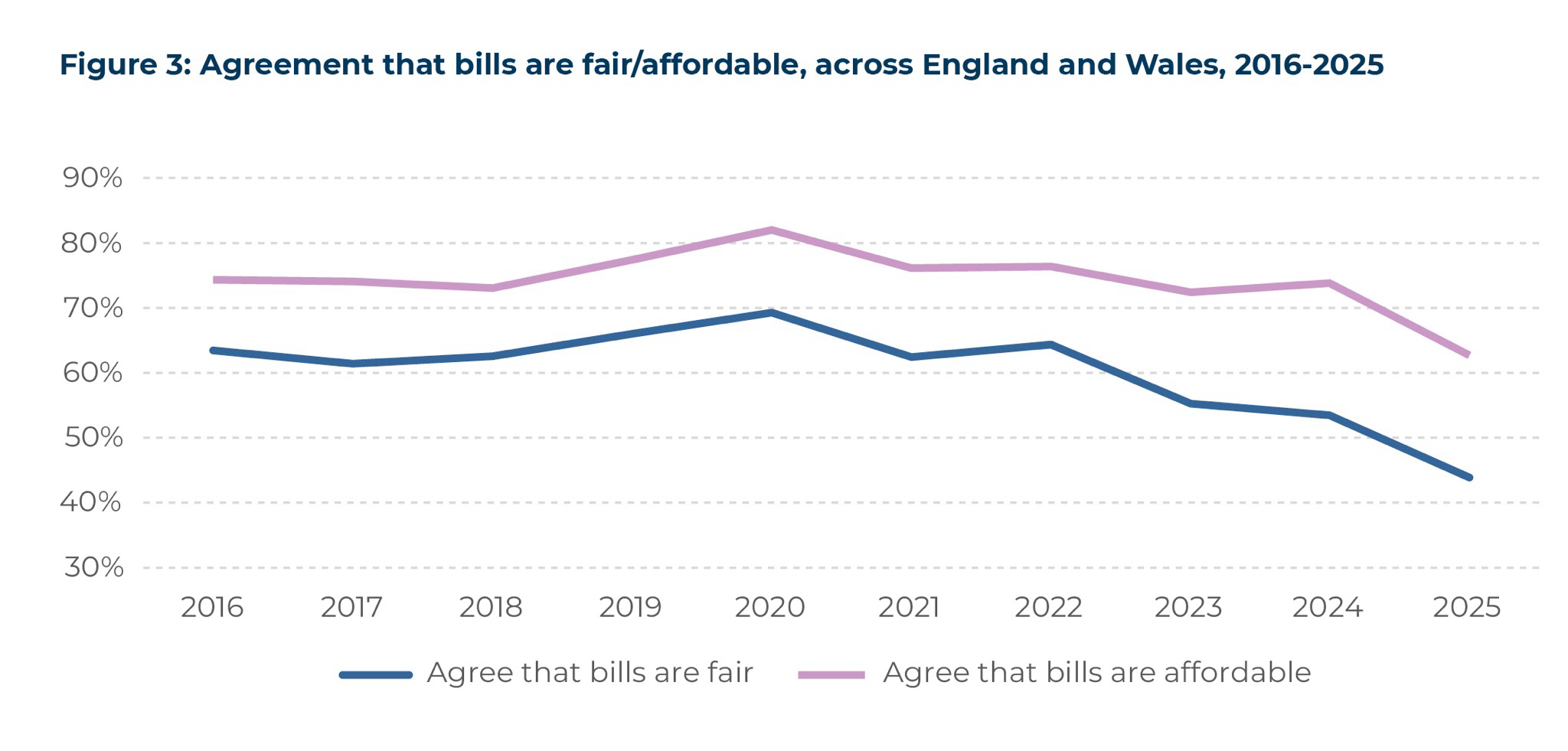

Figure 3: Agreement that bills are fair/affordable, across England and Wales, 2016-2025

There were significant drops in the number of customers who agree their charges are fair and affordable, as figure 3 shows: in both cases, these are far lower than ever before, as well as being the first time fewer than half of customers have agreed that their bill is fair.

However, there has been an increase in awareness of financial support measures – including awareness of WaterSure / WaterSure Wales tariff3 (19% to 25%), and companies’ offers of reduced bills (49% to 56%) – with both now at their highest ever level. We have also seen a record level of customers aware of the Priority Services Register. Our Priority Services Customer Experience and Insights research in December 2025 also identified strong awareness of this service, so it is positive this continues to grow. However, we know from the same research that more needs to be done to increase understanding of all the help available within this service.

Against the backdrop of further bill rises, and increased concern from customers about affordability, it is positive that awareness of vital financial support is continuing to improve. Our Water Worries: Affordability Research in 2025 found that a key barrier in this area was customers lacking awareness of their options, so it is encouraging to see progress being made. However, with the drop in how well customers believe their company communicates services and plans, companies still need to make sure every vulnerable customer knows about the support on offer and can easily access it.

3 WaterSure is a scheme that caps the water bills of metered customers who are in receipt of certain benefit payments and use a lot of water due to 14 a medical condition or having a large family.

Conclusion

This year’s Water Matters results show that the limited improvements we saw in our previous report have not been sustained. In many cases, new record low scores have been seen.

While some companies performed better than others, it is disappointing to see most fared worse across the majority of key metrics. There is not enough progress being made to fundamentally understand and improve communication and delivery of services to customers, so it is time for companies to fully commit to this.

Trust is still the most important thing for companies to work on improving. This continues to decline and most companies saw their score fall. Public scrutiny and concerns around the sector’s environmental performance resulted in customers’ perceptions of sewerage services reaching another record low. This brings into sharp focus the challenge facing companies in restoring consumer trust and where they need to be focusing their attention. Of those companies that saw improvements in trust, three – Northumbrian Water, Bristol Water and South Staffs Water – have seen two consecutive years of improvements since the record industry low in our 2024 report. With the right focus, this shows a turnaround in trust is possible.

After being hit with record bill rises in April 2025, many customers faced further increases this spring. Five companies were also given permission by the Competition and Markets Authority (CMA) in March to increase their customers’ bills beyond the five-year price limits set by Ofwat in December 2024.

All customers need greater clarity and understanding of how their money is being spent. It is also critical struggling households are made aware of the financial support on offer from their water company. That’s why we welcome the increase in awareness of this support, which has surpassed our target of 53% awareness by summer 2026. We have set another ambitious awareness target of 60% in our 2026/27 Forward Work Programme to continue to encourage companies to make sure customers are accessing the right financial support.

It is also vital the support on offer is effective, which is why CCW continues to make the case for a single social tariff for England and Wales. The existing postcode lottery of support needs to be replaced with a single scheme that provides fair and consistent financial help to those who need it most.

Ensuring customers know about, and can access, financial support is vital with bills having climbed to a record high. But companies also need to be far more open about how customers’ money is being spent, and engage with customers, and improve their communication when things go wrong, such as supply interruptions. Companies should also continue to focus on improving their environmental performance as far too many customers remain concerned about sewage pollution.

There is less variance in customers’ perceptions between individual water companies. While some companies are still making progress, the majority are heading in the wrong direction across most key metrics. The Cunliffe Review published last year called for an industry reset to restore public trust in water companies. It is time for companies to commit to this reset and fundamentally rethink their customer communication and delivery of services to reverse the continuing decline in trust and satisfaction.

We will continue to support companies to work collaboratively and encourage the sharing of best practice. Our vulnerability and complaints assessments should help with this turnaround, making sure that companies are addressing complaints properly and supporting vulnerable customers effectively. Our consumer panels will also continue to be an effective way of showing what customers care about and how they want their companies to improve. Providing customers with the opportunity to hold their companies to account can help restore trust and satisfaction, but only if companies act on people’s feedback and keep their promises.

As in previous years, we will be following up this Water Matters report over the coming months with a series of mini reports, looking at different overarching themes from our research in more detail.